The average APR for the benchmark 30-year fixed-rate mortgage rose to 7.26% today from 7.22% yesterday. This time last week, the 30-year fixed APR was 7.22%. Meanwhile, the average APR on a 15-year fixed mortgage is 6.53%. At this same time last week, the 15-year fixed-rate mortgage APR was at 6.45%. And the average APR on the 30-year fixed-rate jumbo mortgage is 7.27%. Last week, it sat at 7.29%

Currently, the average 30-year, fixed-rate mortgage is 6.88% as of March 7, according to Freddie Mac.

While rates remain elevated, the Fed recently signaled that it will begin to cut rates in 2024, indicating a further downward shift in mortgage rates may soon come.

Mortgage Rates Refinance Solutions

Homeowners who are planning to re-finance their home may find the Internet to be a very worthwhile resource. The Internet is useful because it can give the homeowner a wealth of information as well as the ability to compare different rates from different lenders at their convenience.

While these options have made re-financing a more convenient process there is more potential for danger. However, homeowners who exercise a small amount of common sense in using the Internet for re-financing often find they are not at any additional risk.

Comparison Shop at Your Convenience

One of the most popular advantages to researching re-financing online is the ability to comparison shop at the homeowners convenience. This is important because many homeowners work long hours and often find they are not able to meet with lenders during regular business hours because of job restraints. The Internet, however, is open 24 hours a day and allows homeowners to research their options, make important calculations or receive online quotes at any time of the day through the use of automated systems.

Homeowners can also take their time comparing the quotes they receive from these lenders online instead of feeling pressured to provide an immediate response. While homeowners may have some additional time available to them, these same homeowners should realize they do need to act relatively quickly to lock in estimates they receive as interest rates are often time sensitive in nature and cannot be guaranteed for long periods of time.

Use Only Reliable Resources

Homeowners who are using the Internet to research re-financing options and obtain quotes should carefully consider their sources when making important decisions regarding the subject of re-financing. Homeowners who stick with well known lenders and established websites will not likely encounter problems but those who select a new lender may be surprised by the results of the re-financing attempt.

Homeowners who are unsure about the reliability of a particular resource or lender should do additional research on the company. One of the easiest ways to do this is to consult the Better Business Bureau (BBB). The BBB may be able to provide the homeowner with valuable information regarding the number of previous complaints against the company.

A company who has a large number of unresolved complaints should be considered an unreliable company. However, homeowners should not assume companies without a significant number of complaints are reputable unless the company has been in existence for a number of years and is a member of the BBB.

Homeowners should also take care not to be fooled by fancy web design. A website which looks very professional is not necessarily a website which is accurate and informative. Many skilled website designers can create websites which are both attractive and professional looking.

These website designers can also optimize a website for particular mortgage related keywords so users find the page easily when searching for these terms but this does not necessarily make the website designer knowledgeable about the subject to re-financing.

Confirm Loan Terms in Person before Committing

While shopping for re-financing options online is certainly easy and convenient, homeowners should consider completing the application process either in person or over the phone instead of relying on an automated system.

While the Internet is good for research purposes, homeowners can take advantage of face to face meetings or telephone conferences to ask all of their relevant questions. Asking all of these questions will help the homeowner to ensure he fully understand the loan terms as well as all of his available options.

Completing the re-financing process in person or over the phone can also prevent the homeowner from being surprised by any elements of the mortgage re-finance. This may include additional fees which are tacked on during the processing of the application, rates which are only available in certain situations or other elements of the re-financing agreement which could significantly impact the homeowners decision making process.

Understanding Refinancing

Understanding the process of re-financing can be quite dizzying. Homeowners who are considering re-financing might initially be overwhelmed by the number of options available to them. However, after taking some time to educate themselves about the process, they will likely find the process is not nearly as daunting as they had imagined. This article will discuss some of the options available to those interested in re-financing as well as some of the important factors to consider in order to determine whether or not refinancing is worthwhile.

Consider the Options

Homeowners have quite a few options available to them when they are considering the possibility of re-financing their home. The most significant decision is the type of loan they will choose. Fixed rate mortgages and adjustable rate mortgages (ARMs) are the two main types of mortgages the homeowners will likely encounter. Additionally there are hybrid loan options available.

As the name implies, a fixed rate mortgage is one in which the interest rate remains constant throughout the duration of the loan period. This is an especially favorable type of loan when the homeowner has credit which is sufficient enough to lock in a low interest rate.

ARMs are mortgages where the interest rate varies during the course of the loan period. The interest rate is usually tied to an index such as the prime index and is subject to rises and falls in accordance with this index. This is considered a riskier type of loan and is therefore often offered to homeowners who have less favorable credit scores.

Although ARMs are considered somewhat risky there is usually a certain degree of protection written into the loan agreement. This may come in the form of a clause which limits the amount the interest rate can increase, in terms of percentage points, over a fixed period of time. This can protect the homeowner from sharp increases in the interest rates which would otherwise considerably raise the amount of their monthly payments.

Hybrid loans are mortgages which combine a fixed element with an adjustable element. An example of this type of loan is a situation where the lender may offer a fixed interest rate for the first five years of the loan and a variable interest rate for the remainder of the loan. Lenders typically offer a lower introductory interest rate for the fixed period to make the mortgage seem more enticing.

Consider the Closing Costs

The closing costs associated with re-financing should be carefully considered when deciding whether or not to re-finance the home. This is significant because when homeowners re-finance their home they are often subject to many of the same closing costs as when they originally purchased the home. These costs may include, but are not limited to appraisal fees, application fees, loan origination fees and a host of other expenses. These costs can be quite significant. The closing costs will be significant when the homeowner considers the overall savings associated with re-financing.

Consider the Overall Savings

When deciding whether or not to re-finance, the overall savings is one factor the homeowners should carefully consider. This is important because re-financing is typically not considered worthwhile unless it results in a financial savings. Although some homeowners refinance to lower monthly costs and are not concerned with the overall picture, most homeowners consider whether or not they will be saving money by refinancing.

The amount of money the homeowner will save when re-financing is largely dependent on the new interest rate in relation to the old interest rate. Other factors come into play such as the remaining balance of the existing loan as well as the amount of time the homeowner intends to stay in the home before selling the property. It is important to note that the amount of money saved by negotiating a lower interest rate is not equal to the entire savings.

The homeowner must determine the closing costs associated with re-financing and subtract this sum from the potential savings. A negative number would indicate the new interest rate is not low enough to offset the closing costs. Conversely a positive number indicates an overall savings. With this information the homeowner can decide whether or not he wishes to re-finance.

How To Get a Cash Out Re-Finance?

A cash out re-finance basically enables the homeowner to re-finance their home for an amount greater than the balance of the exiting mortgage. The homeowners than repay the existing balance plus the additional amount over the course of the loan period and are given a check for the amount above and beyond the balance of the exiting mortgage. The homeowners can use this check for any purpose they choose now and repay the debt along with the rest of re-financed amount.

When is a Cash Out Re-Finance possible?

A cash out option is available when there is existing equity in the home. This is important because the lender is able to justify the practice of offering increased funds to the homeowner due to the value of the property. This is because the lender feels as though the security of having the home for collateral does not put them at a high risk for the homeowner defaulting on the loan.

Homeowners who wish to take advantage of a cash out re-finance offered by a lender should inquire as to whether or not the lender offers this type of re-financing. This is important because not all lenders offer this option. It should actually be one of the first questions the homeowner asks when inquiring about re-financing programs. Doing so will save homeowners, who are seeking a cash out re-finance, a great deal of time.

How Can the Cash be Used?

For many homeowners the most appealing aspect of cash out re-financing is that the additional funds can be used for any purpose desired by the homeowner. The homeowner does not even have to offer the lender an explanation of how the additional funds will be used. This is important because once the lender writes the check for the additional funds, he has no concern for how the money is used. This is because the amount of the additional funds is rolled into the re-financed mortgage. The lender simply focuses on the homeowners ability to repay the mortgage and is not concerned with how the homeowner uses the funds which are released in the cash out.

While the purpose of a cash out re-finance does not have to be disclosed to the lender, the homeowner would be wise to use these funds in a judicious manner. This is because the homeowner will be responsible for repaying these funds to the lender. Some of the popular uses for funds collected from cash out re-financing include:

* Undertaking home improvement projects

* Purchasing items for the home

* Taking a dream vacation

* Putting money in a childs tuition fund or

* Purchasing a vehicle

* Starting a small business

All of the reasons listed above are excellent uses of a cash out re-finance option. Homeowners who are considering this type of a re-financing option should also consider whether or not the deductions are tax deductible. Using the cash out option to make home improvements is jus one example of a situation where the funds can be tax deductible. Homeowners should consult their tax attorney on the matter to determine whether or not they are able to deduct the interest from the repayment of their re-financing loan.

Cash Out Re-Financing Example

The process of a cash out refinancing option is fairly easy to illustrate with a simple example. Consider a homeowner who purchases a $150,000 with a 7% interest. Now consider the homeowner has already repaid $50000 of the loan and would like to borrow an additional $20,000 to make a rather large purchase or invest in a small business.

With this additional funding available the homeowners have the opportunity to use the equity in their home to make their dreams come true. In the example above the homeowner may refinance for a total of $120,000 at a lower interest rate such as 6.25%. This process allow the homeowner to take advantage of the existing equity in their home and also allows the homeowner to qualify for a substantial loan at a rate typically reserved for re-financing or home loans.

Benefits of Re-Financing

There are a number of benefits which may be associated with re-financing a home. While there are some situations where re-financing is not the right decision, there are a host of benefits which can be gained from re-financing under favorable conditions. Some of these benefits include lower monthly payments, debt consolidation and the ability to utilize the existing equity in the home. Homeowners who are considering re-financing should consider each of these options with their current financial situation to determine whether or not they wish to re-finance their home.

Lower Monthly Payments

For many homeowners, the possibility of lower monthly payments is a very appealing benefit of re-financing. Many homeowners live paycheck to paycheck and for these homeowners finding an opportunity to increase their savings can be a monumental feat. Homeowners who are able to negotiate lower interest rates when they re-finance their home will likely see the benefit of lower monthly mortgage payments resulting from the decision to re-finance.

Each month homeowners submit a mortgage payment. This payment is typically used to repay a portion of the interest as well as a portion of the principle on the loan. Homeowners who are able to refinance their loan at a lower interest rate may see a decrease in the amount they are paying in both interest and principle. This may be due to the lower interest rate as well as the lower remaining balance. When a home is re-financed, a second mortgage is taken out to repay the first mortgage. If the existing mortgage was already a few years old, it is likely the homeowner already had some equity and had paid off some of the previous principle balance. This enables the homeowner to take out a smaller mortgage when they re-finance their home because they are repaying a smaller debt than the original purchase price of the home.

Debt Consolidation

Some homeowners begin to investigate re-financing for the purpose of debt consolidation. This is especially true for homeowners who have high interest debts such as credit card debts. A debt consolidation loan enables the homeowner to use the existing equity in their home as collateral to secure a low interest loan which is large enough to repay the existing balance on the home as well as a number of other debts such as credit card debt, car loans, student loans or any other debts the homeowner may have.

When re-financing is done of the purpose of debt consolidation there is not always an overall increase in savings. Those who are seeking to consolidate their debts are often struggling with their monthly payments and are seeking an option which makes it easier for the homeowner to manage their monthly bills.

Additionally, debt consolidation can also simplify the process of paying monthly bills. Homeowners who are apprehensive about participating in monthly bill pay programs may be overwhelmed by the amount of bills they have to pay each month. Even if the value of these bills is not worrisome just the act of writing several checks each month and ensuring they are sent, on time, to the correct location can be overwhelming. For this reason, many homeowners often re-finance their mortgage to minimize the amount of payments they are making each month.

Using the Existing Equity in the Home

Another popular reason for re-financing is to use the existing equity in the home. Homeowners who have a considerable amount of equity in their home may find they are able to cash out some of this equity for other purposes. This may include making improvements to the home, starting a business, taking a dream vacation or pursuing a higher degree of education.

The homeowner is not limited in how they can use the equity in their home and may re-finance a home equity line of credit which can be used for any purpose imaginable. A home equity line of credit is different from a loan because the funds are not disbursed all at once. Rather the funds are made available to the homeowner and the homeowner can withdraw these finds at anytime during the draw period.

Is It Time to Re-Finance?

Whether or not to re-finance is a question homeowner may ask themselves many times while they are living in their home. Re-financing is essentially taking out one home loan to repay an existing home loan. This may sound odd at first but it is important to realize when this is done properly it can result in a significant cost savings for the homeowner over the course of the loan. When there is the potential for an overall savings it might be time to consider re-financing. There are certain situations which make re-financing worthwhile. These situations may include when the credit scores of the homeowners improve, when the financial situation of the homeowners improves and when national interest rates drop. This article will examine each of these scenarios and discuss why they may warrant a re-finance.

When Credit Scores Improve

There are currently so many home loan options available, that even those with poor credit are likely to find a lender who can assist them in realizing their dream of purchasing a home. However, those with poor credit are likely to be offered unfavorable loan terms such as high interest rates or variable interest rates instead of fixed rates. This is because the lender considers these homeowners to be higher risk than others because of their poor credit.

Fortunately for those with poor credit, many credit mistakes can be repaired over time. Some financial blemishes such as bankruptcies simply disappear after a number of years while other blemishes such as frequent late payments can be minimized by maintaining a more favorable record of repaying debts and demonstrating an ability to repay existing debts.

When a homeowners credit score improves considerable, the homeowner should inquire about the possibility of re-financing their current mortgage. All citizens are entitled to a free annual credit report from each of the three major credit reporting bureaus. Homeowners should take advantage of these three reports to check their credit each year and determine whether or not their credit has increased significantly. When they notice a significant increase, they should consider contacting lenders to determine the rates and terms they may be willing to offer.

When Financial Situations Change

A change in the homeowners financial situation can also warrant investigation into the process of re-financing. A homeowner may find himself making considerably more money due to a change in jobs or considerably less money due to a lay off or a change in careers. In either case the homeowner should investigate the possibility of re-financing. The homeowner may find an increase in pay may allow them to obtain a lower interest rate.

Alternately a homeowner who loses their job or takes a pay cut as a result of a change in careers may hope to refinance and consolidate their debt. This may result in the homeowner paying more because some debts are drawn out over a longer period of time but it can result in a lower monthly payment for the homeowner which may be advantageous at this juncture of his life.

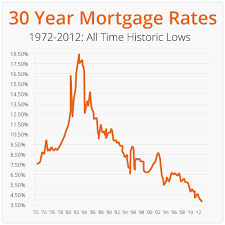

When Interest Rates Drop

Interest rates dropping is the one signal that sends many homeowners rushing to their lenders to discuss the possibility of re-financing their home. Lower interest rates are certainly appealing because they can result in an overall savings over the course of the loan but homeowners should also realize that every time the interest rates drop, a re-finance of the home is not warranted. The caveat to re-financing to take advantage of lower interest rates is that the homeowner should carefully evaluate the situation to ensure the closing costs associated with re-financing do not exceed the overall savings benefit gained from obtaining a lower interest rate. This is significant because if the cost of re-financing is higher than the savings in interest, the homeowner does not benefit from re-financing and may actually lose money in the process.

The mathematics associated with determining whether or not there is an actual savings is not overly complicated but there is the possibility that the homeowner will make mistakes in these types of calculations. Fortunately there are a number of calculators available on the Internet which can help homeowners to determine whether or not re-financing is worthwhile.

How Today’s Mortgage Rates Affect Your Monthly Payments

If you know how much you’re borrowing, what type of loan you’re getting and how many years you have to pay it back, you can use a mortgage calculator to check your monthly payment at different interest rates.

For instance, if you have a starting loan balance of $425,000 on a 30-year fixed-rate mortgage, here’s approximately what you can expect to pay in principal and interest every month, excluding taxes, insurance and HOA fees:

- At a 5% interest rate. $2,281 in monthly payments (excluding taxes, insurance and HOA fees)

- At a 6% interest rate. $2,548 in monthly payments (excluding taxes, insurance and HOA fees)

- At a 7% interest rate. $2,828 in monthly payments (excluding taxes, insurance and HOA fees)

- At an 8% interest rate. $3,119 in monthly payments (excluding taxes, insurance and HOA fees)

How To Get the Best Mortgage Rate Today

Though lenders decide your mortgage rate, there are some proactive steps you can take to ensure the best rate possible. For example, advanced preparation and meeting with multiple lenders can go a long way. Even lowering your rate by a few basis points can save you money in the long run.

Here are some other ways you can improve your chances of getting the best deal:

- Take stock of your financial situation. Before you fall in love with your dream home, you better make sure you can afford the monthly payments and other homeownership costs. For instance, start by looking at your debt-to-income (DTI) ratio—aka your total monthly debts against your monthly earnings—to determine how much home you can afford.

- Review your credit score. Lenders look at your credit score to evaluate the risk you pose as a borrower. A higher score gives you a better chance at scoring favorable mortgage terms. Paying down balances, limiting new credit cards and loans and checking your credit report for errors can all work towards raising your score.

- Meet with several lenders. Don’t go with the first lender quote you receive. Shop around to get the best deal—research various mortgage lenders and different loans you might qualify for to put yourself in a stronger position once you are ready to buy a home.

- Crunch the numbers with a mortgage calculator. Once you know which type of loan you qualify for, you can estimate your monthly payments by punching your numbers into various mortgage calculators, such as a 30-year fixed mortgage calculator or mortgage amortization calculator.

- Save money. The more you put down on a home, the less you’ll need to borrow from a lender. This means lower monthly payments and more savings over the life of the loan.

What Affects Current Mortgage Rates?

Mortgage rates are indirectly influenced by the Federal Reserve’s monetary policy. When the central bank raises the federal funds target rate, as it did throughout 2022 and 2023, that has a knock-on effect by causing short-term interest rates to go up. In turn, interest rates for home loans tend to increase as lenders pass on the higher borrowing costs to consumers.

In addition to monetary policy, lenders also have an impact on mortgage rates. A lender with physical locations and a lot of overhead may charge higher interest rates to cover its operating costs and make a profit on its mortgage business. On the other hand, lenders that operate solely online, tend to offer lower mortgage rates because they have less fixed costs to cover.

Finally, your individual credit profile also affects the mortgage rate you qualify for. Borrowers with a strong credit history and good score (at least 670) usually receive a lower interest rate, while borrowers with a poor credit score—who lenders consider high risk—are typically charged a higher interest rate.

I am known as Fredrick Biggs I am a writer and an industrialist by profession. My age is 30 years. My aim is to gather the attention of the targeted audience without being boring and unexciting.

I like to utilize the free time in writing my views and thoughts for my book lovers or readers. My most preferred articles are usually about services sector and business; however, I have written various topics in my articles. I do not have a specific genre.